When was the last time you left the house without your smartphone? If just the thought of that makes you feel uneasy, you are not alone. Nearly three-quarters of all Americans are in the same boat. Smartphone adoption is long past its infancy with about 90% of the global population owning a smartphone, and we’re using them for much more than just calling family or scrolling through social media. This technological advancement leads us into the realm of mobile commerce—the act of shopping from your cellphone—which now accounts for an estimated 68% of all retail sales. Why has this become such a sweeping trend? Because it’s quicker and easier than remembering your credit card every time you want to shop, making it a game-changer for both consumers and retailers alike.

Mobile payment processing allows retailers to capitalize on the shift to mobile within their stores. This guide will explore how to implement mobile payment systems by 2025, the technology you’ll need, and the various types of mobile payments you can accept.

1. Customer Sets Up Their Digital Wallet

A digital wallet is an electronic payment method that customers use to pay for products via their smartphone. This first step is critical because it lays the groundwork for all subsequent mobile transactions. Customers can use their smartphone’s native wallet like Apple Pay, Google Pay, or Samsung Pay. By 2027, it is estimated by Statista that more than one-third of all U.S. retail sales will be made using digital wallets. This is a stark increase from just 10% in 2020, driven by the convenience that mobile wallets offer. They eliminate the need for customers to remember their payment details each time they want to make a purchase and the necessity to carry a physical card.

Customers are also reassured by the security features of mobile wallets. For example, when a customer pays for their order in-store using Apple Pay, the retailer does not see their debit or credit card number. The wallet tokenizes those details to maintain the user’s privacy. This reduces the risk of fraudulent activities and protects sensitive customer data.

2. They Link Their Bank Account or Credit Card

Once the digital wallet is set up, the next step is to link it with a bank account or credit card. This setup phase is crucial as it ties the digital wallet to actual funds. Linking the wallet to a bank account or credit card is a simple process for customers, often requiring just a few taps on their smartphone. These payment methods mirror the traditional ones but offer more convenience and security.

This functionality is enhanced with extra layers of security, such as two-factor authentication, fingerprint, or facial recognition methods. These features make it easier for consumers to adopt mobile payment methods because they feel their financial data is protected. For retailers, this means fewer obstacles to get customers on board with new payment systems, making the shift smoother and more effective.

3. The Customer Visits a Retail Store or Starts an Online Purchase

With their digital wallet set up and linked to a bank account or credit card, customers can now visit a retail store or begin an online purchase. For retailers, this means preparing for a seamless checkout process that handles both in-store and online transactions fluidly. The shift to mobile payments is not only about convenience but also about meeting customers where they are, whether physically in the store or virtually online.

Retailers should ensure their POS systems are capable of accepting mobile payments both online and offline. This unification across touchpoints can significantly enhance customer satisfaction by offering them the flexibility to complete transactions however they prefer. This move towards a more integrated system is vital for the future of retail, where the lines between online and offline shopping continue to blur.

4. In-Store, They Tap Their Smartphone on NFC-Enabled Mobile Card Readers

Near-field communication (NFC) is a cornerstone technology in mobile payment processing. When a customer taps their smartphone on an NFC-enabled mobile card reader in-store, the payment information is transmitted securely via radio waves. NFC technology makes mobile payments fast, easy, and secure, providing a win-win scenario for both consumers and retailers.

To capitalize on this, retailers need to equip their stores with NFC-enabled mobile card readers. Many current POS systems already support NFC, but it is crucial to verify and upgrade if necessary. Adopting NFC technology is not just advantageous for customer convenience; it also opens up new opportunities for streamlining the checkout process. This can significantly reduce wait times, making the in-store shopping experience smoother and more enjoyable.

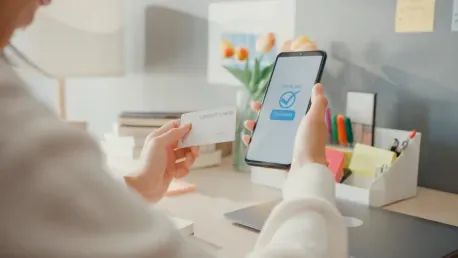

5. Online, They Open the Wallet and Approve the Transaction

In online scenarios, customers simply open their digital wallet to approve the transaction. This approval often involves advanced security features like biometrics, which offer an extra layer of protection. For retailers, integrating this seamless approval process into their ecommerce platforms can make a big difference in conversion rates and customer satisfaction.

Customers are increasingly looking for quick and secure ways to shop online, and the ability to use their digital wallets addresses this need perfectly. Offering mobile payment options online not only caters to customer preference but also improves the speed and accuracy of transactions. Retailers who fail to adapt to this trend risk losing out to competitors who offer a more streamlined and secure online shopping experience.

6. The Transaction Is Processed and Finalized

The final step in the mobile payment process is the transaction itself, which is processed and finalized almost instantaneously. Mobile payments are designed to be fast and efficient, reducing the time customers spend at checkout. This immediacy benefits not only customers but also retailers, who can handle more transactions in a given timeframe and improve overall sales efficiency.

For retailers, the beauty of mobile payment processing lies in its ability to provide a quick, secure, and convenient shopping experience for customers. By implementing the steps outlined, retailers can set themselves up for success in the coming years. A robust mobile payment system can significantly enhance customer satisfaction, streamline in-store operations, and offer invaluable data insights for future business strategies.

With the convenience, security, and speed that mobile payments offer, it is clear why they have seen such rapid adoption. As retailers look toward the future, those who embrace mobile payment technology will undoubtedly be better positioned to meet the evolving needs of their customers and stay competitive in an increasingly digital marketplace.

Actionable Next Steps for Retailers

Retailers looking to implement mobile payment processing by 2025 should start with a thorough evaluation of their current payment systems. Identify gaps and areas for improvement, and choose a reliable merchant services provider that offers PCI compliance, fair pricing, essential integrations, robust customer support, and scalability. Setting up the appropriate hardware and software is equally crucial. Investing time in training staff to handle mobile payments efficiently can prevent potential hiccups and ensure a seamless customer experience.

Future Considerations

In the realm of online shopping, customers can easily approve transactions by opening their digital wallets. This process often includes advanced security measures such as biometrics, adding an extra layer of protection. For retailers, incorporating this hassle-free approval process into their e-commerce platforms can significantly boost conversion rates and enhance customer satisfaction.

Consumers today are increasingly seeking quick and secure ways to make online purchases, and digital wallets perfectly address this need. By offering mobile payment options, online retailers not only meet customer preferences but also enhance the speed and accuracy of transactions. Retailers who ignore this trend risk losing business to competitors who provide a more efficient and secure online shopping experience.

Incorporating digital wallets into online shopping platforms is more than just a convenience; it is becoming a standard that customers expect. The use of biometrics like facial recognition or fingerprints for approval not only speeds up the checkout process but also reduces the likelihood of fraud. This dual benefit of security and efficiency is crucial in today’s competitive e-commerce landscape. Retailers who adapt to these changing customer expectations can gain a significant edge, while those who don’t may find themselves falling behind, losing both trust and sales. The shift toward digital wallets is not just a fleeting trend but a permanent change in how consumers prefer to shop online.